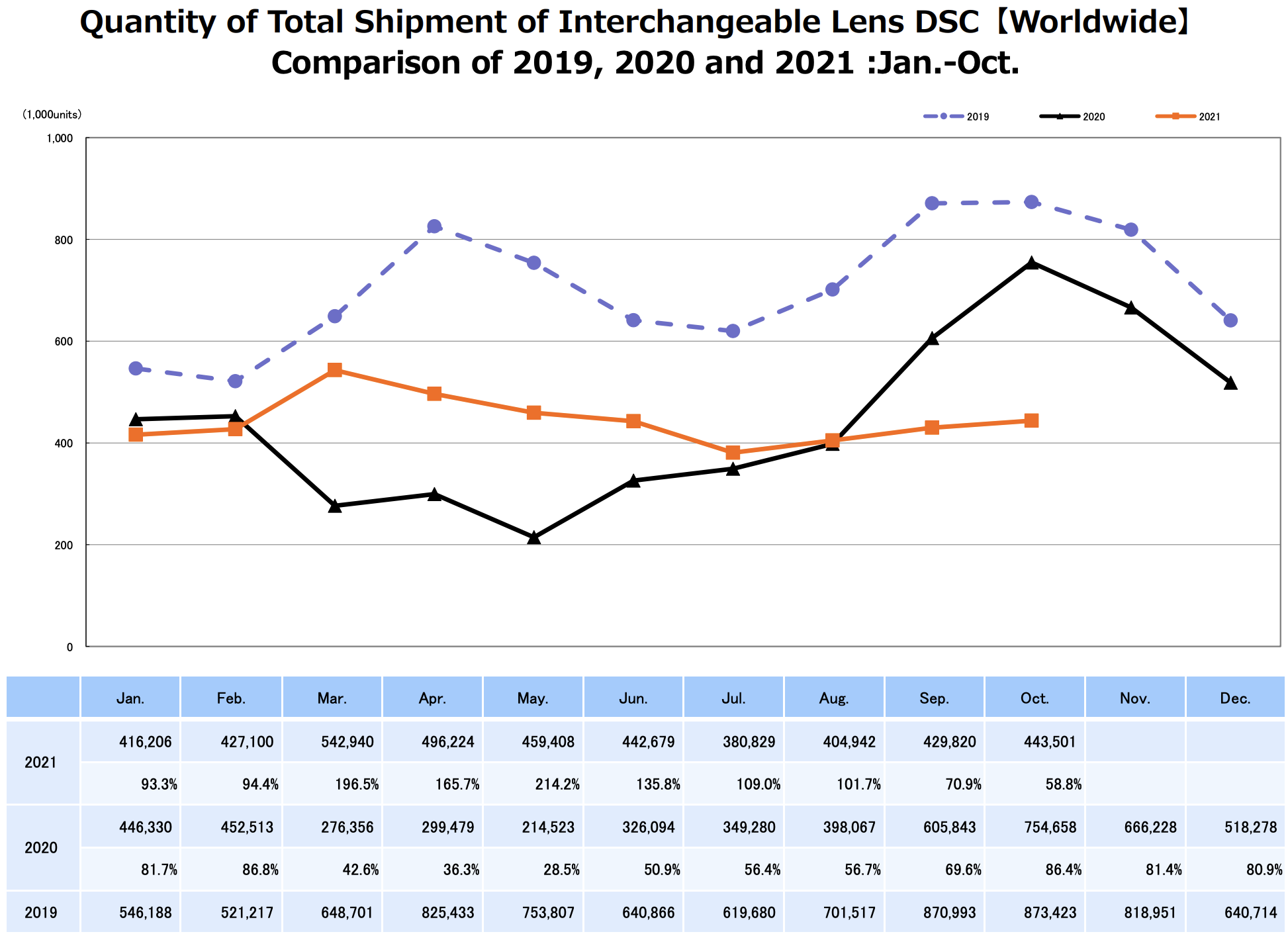

The CIPA October 2021 numbers are out (orange: 2021, black: 2020, blue: 2019):

October 2021 CIPA numbers

September DSLR and Mirrorless body shipments for the month were ahead of September 2021, but substantially behind last October. For the month, DSLR units were down 45.5% and Mirrorless units were down 37.8% as compared to October 2020.

Mirrorless now has a 58% unit share of ILC’s and a 77.2% shipped value share (of DSLR + Mirrorless).

Based on the first ten months of 2021 and last year’s shipping patterns, we predict a full year estimate of 5.3 to 5.7 million ILC units shipped compared to:

That’s down substantially from our last estimate unless November shipments picked up for the holiday season (Canon has predicted a full fiscal year industry estimate of 6 million units and they claim they’ll take 50% of that).

October 2021 Calendar year-to-date Units & Shipped Value:

(All comparisons to Jan-October 2020)

DSLR Units : 1867K –2% YTD

DSLR Shipped Value: ¥76.5 billion –1% YTD

Mirrorless Units: 2577K +16% YTD

Mirrorless Shipped Value: ¥258 billion +42% YTD

Compact Units: 2499K –13% YTD

Compact Shipped Value: ¥59.8 billion -4% YTD

Lenses for smaller than 35mm Units: 4178K –3% YTD

Lenses for smaller than 35mm Shipped Value: ¥64.4 billion +4% YTD

Lenses for 35mm and larger Units: 3733K, +31% YTD

Lenses for 35mm and larger Shipped Value: ¥212.1 billion +52% YTD

Cumulative YTD Mirrorless unit share (of Mirrorless + DSLR): 58% (was 53.9% Jan-Oct 2020)

Cumulative YTD Mirrorless Shipped Value share: 77.2% (was 70.2% Jan-Oct 2020)

The ratio of lenses shipped to bodies shipped is 1.78 for Jan-Oct 2021. It was 1.73 for Jan-Sept 2020.

October 2021 Calendar year-to-date Geographic Share:

DSLR:

Mirrorless:

Compacts:

Lenses:

List of participating CIPA companies can be found here.

Source: CIPA (thanks ZoetMB) via NikonRumors

{kind=link}

{kind=link}

{kind=link}

{kind=link}