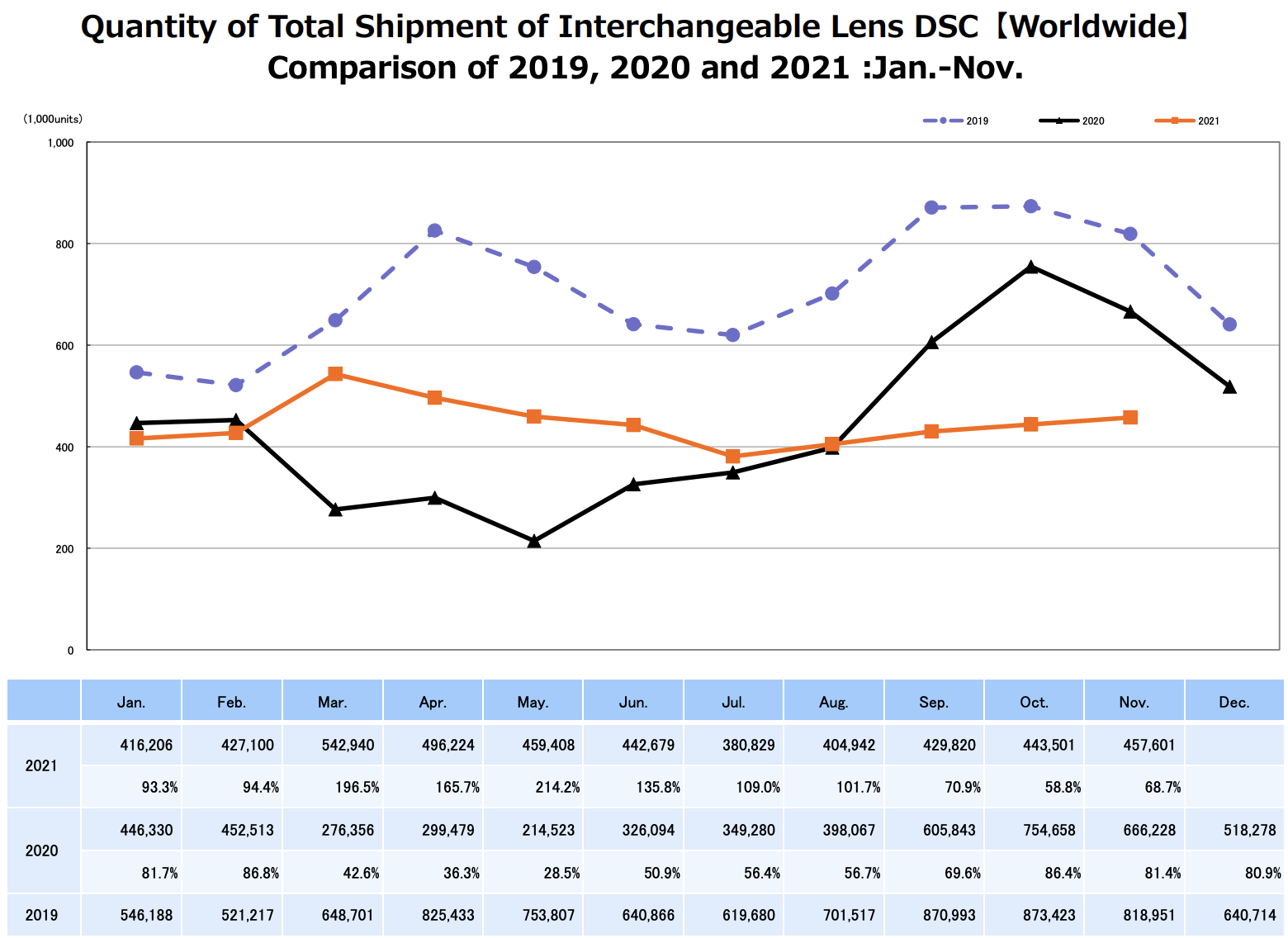

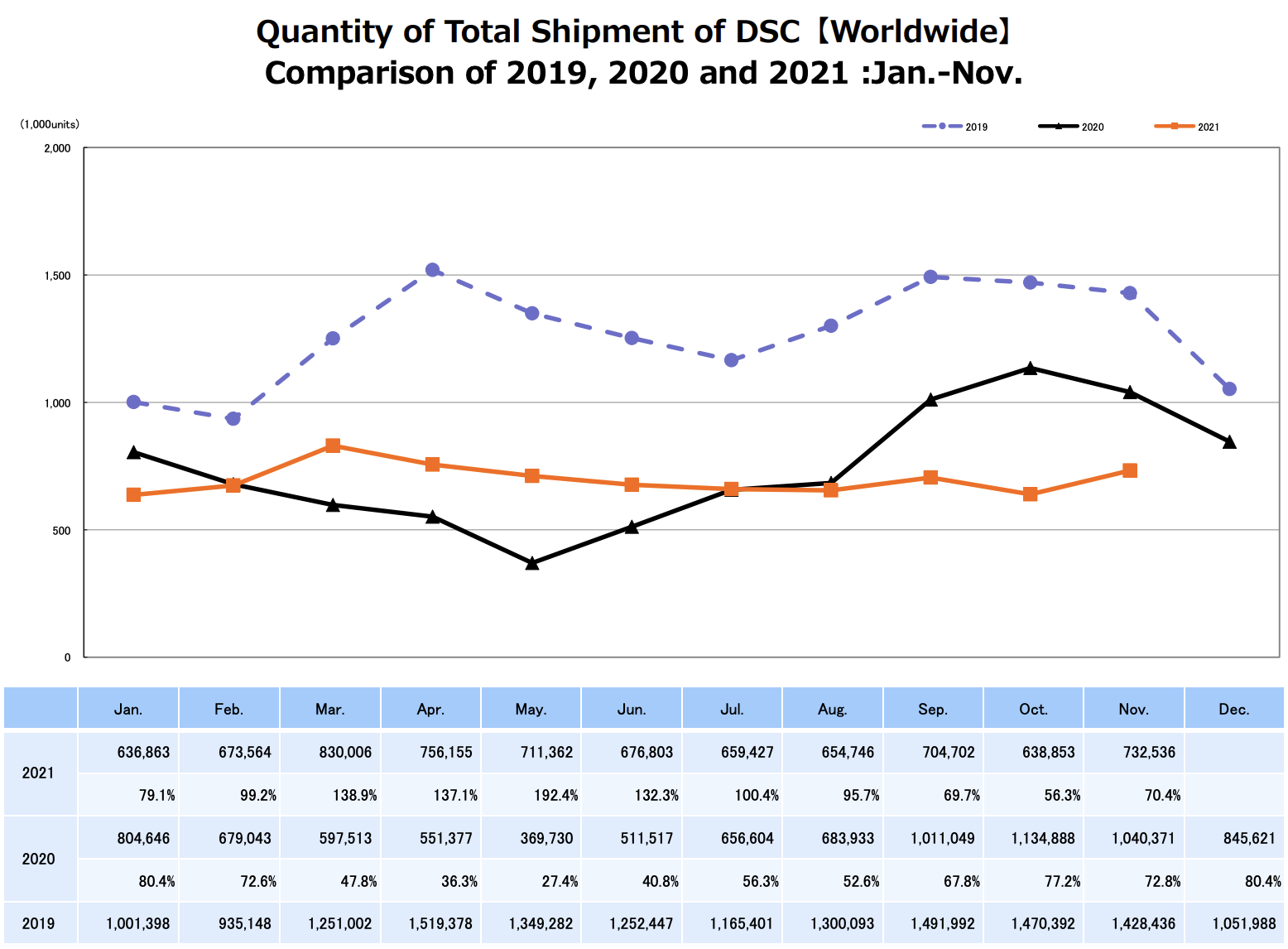

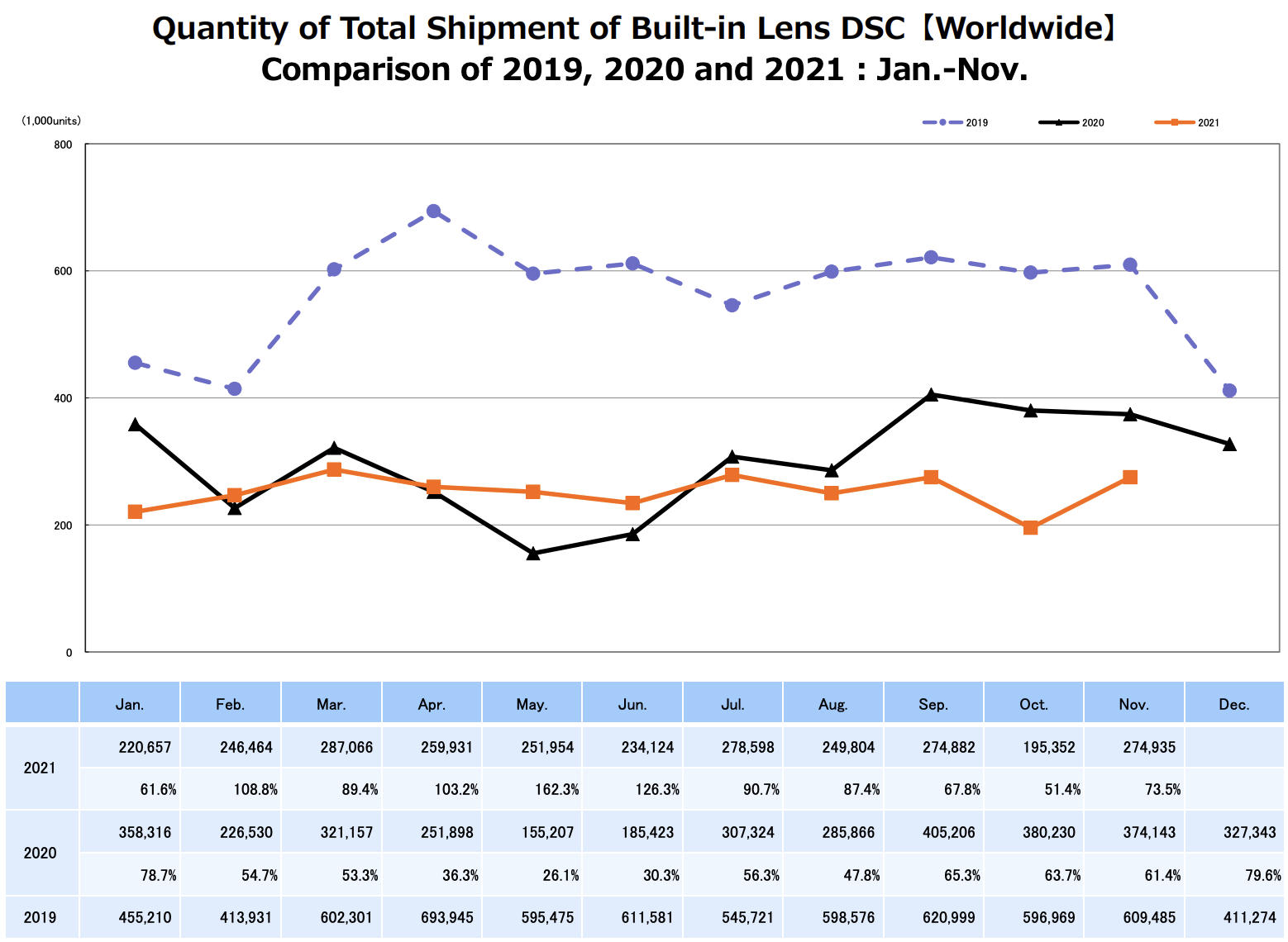

The CIPA camera production data for November 2021 is out (orange: 2021, black: 2020, blue: 2019):

November 2021 CIPA numbers

Except for full frame camera lenses, everything was down substantially from November 2020 (single month). Cumulatively for the year, Mirrorless is up, full frame lenses is up and smaller than full frame lenses shipped value is up (but not units), but everything else is down.Mirrorless now has a 59% unit share of ILC’s and a 78% shipped value share (of DSLR + Mirrorless).

Based on the first eleven months of 2021 and last year’s shipping patterns, we predict a full year estimate of 5.346 to 5.432 million ILC units shipped compared to:

which means that 2021 won’t come in much better than 2020 and if little shipped in December, it could actually be worse.

(Canon had predicted a full fiscal year industry estimate of 6 million units and they claim they’ll take 50% of that, but it looks like they estimated too high.)

November 2021 Calendar year-to-date Units & Shipped Value (all comparisons to Jan-November 2020):

DSLR Units : 2028K –7% YTD

DSLR Shipped Value: ¥83.2 billion –5% YTD

Mirrorless Units: 2873K +10% YTD

Mirrorless Shipped Value: ¥297 billion +37% YTD

Compact Units: 2774K –15% YTD

Compact Shipped Value: ¥67.15 billion -4% YTD

Lenses for smaller than 35mm Units: 4554K –8% YTD

Lenses for smaller than 35mm Shipped Value: ¥70.8 billion +2% YTD

Lenses for 35mm and larger Units: 4190K, +29% YTD

Lenses for 35mm and larger Shipped Value: ¥240.2 billion +51% YTD

Cumulative YTD Mirrorless unit share (of Mirrorless + DSLR): 58.6% (was 54.5% Jan-Nov 2020)

Cumulative YTD Mirrorless Shipped Value share: 78.1% (was 71.1% Jan-Nov 2020)

The ratio of lenses shipped to bodies shipped is 1.78 for Jan-Nov 2021. It was 1.71 for Jan-Nov 2020.

November 2021 Calendar year-to-date Geographic Share:

DSLR:

Mirrorless:

Compacts:

Lenses:

List of participating CIPA companies can be found here.

Source: CIPA (thanks ZoetMB)

Via NikonRumors

{kind=link}

{kind=link}

{kind=link}