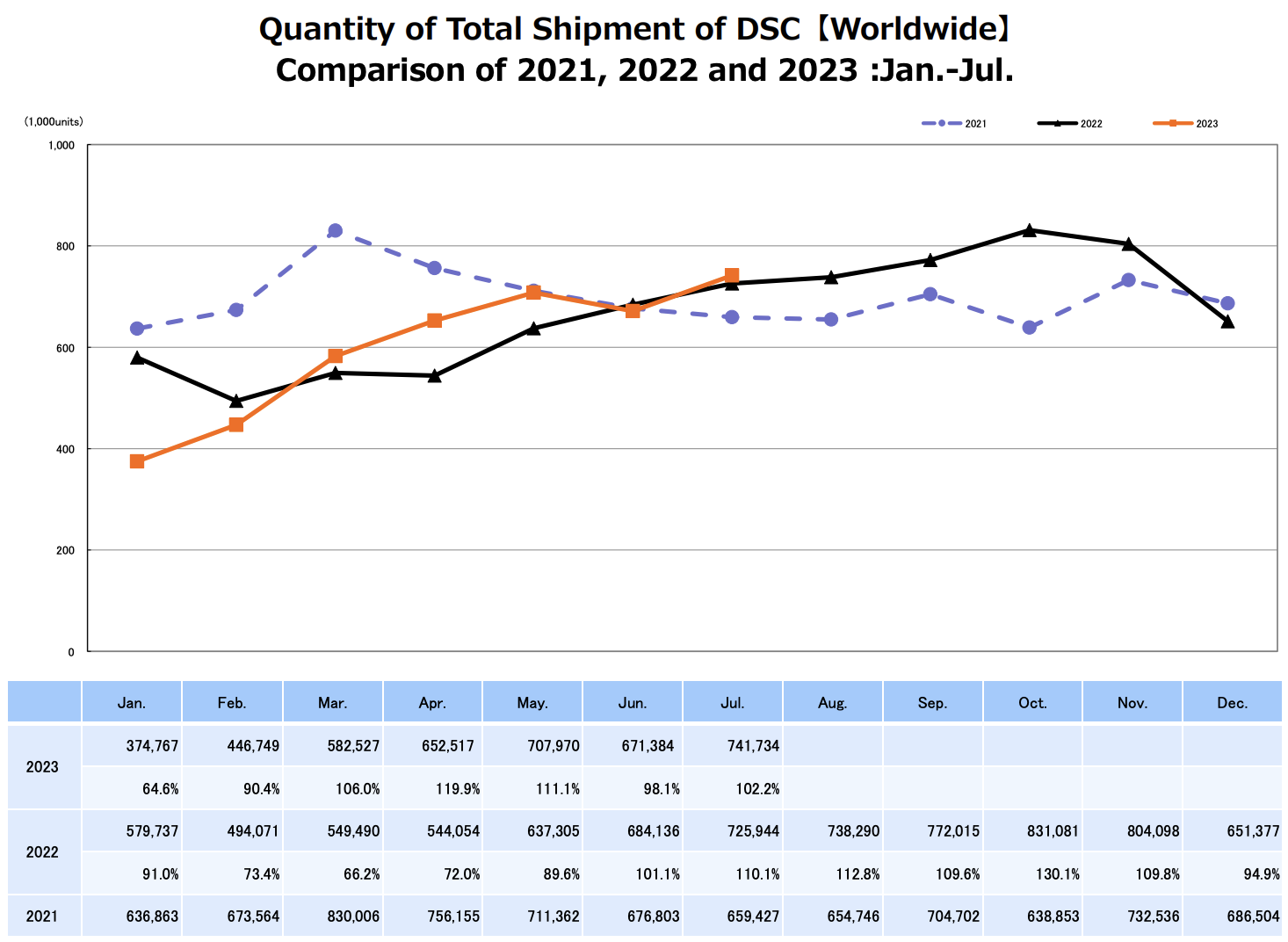

CIPA (Camera & Imaging Products Association in Japan) published their latest camera production data (orange: 2023, black: 2022, blue: 2021):

July 2023 CIPA numbers by ZoetMB

July shipped units were the best of the year for DSLRs and Mirrorless bodies and 2nd best of the year for compacts, although a little ground was lost on cumulative mirrorless units compared to YTD last year and mirrorless body share inexplicably dropped slightly by 0.3%. Shipped value was the best of the year for DSLRs and 2nd best of the year for Mirrorless.

CIPA predicted 5.72 million DSLR and Mirrorless bodies and 9.39 million lenses for calendar 2023. We’re predicting 5.5 to 6m bodies, slightly more than last month on the low end,

That compares to:

2022: 5.927 million bodies (+10.8%), 9.7 million lenses (+1.6%).

2021: 5.348 million bodies (+0.75%), 9.55 million lenses (+6.1%)

2020: 5.308 million bodies (-37.3%), 9 million lenses (-36.6%)

2019: 8.462 million bodies (-21.4%), 14.2 million lenses (-21.1%)

2018: 10.76 million bodies (-7.9%), 18 million lenses (-6.4%)

2017: 11.68 million bodies (+0.6%) 19.22 million lenses (+0.156%)

2016: 11.61 million bodies (-11.1%), 19.19 million lenses (-11.6%)

2015: 13.06 million bodies (-5.6%), 21.7 million lenses (-5.2%)

2014: 13.84 million bodies (-19.2%), 22.9 million lenses (-14.2%)

2013: 17.13 million bodies (-15%), 26.7 million lenses (-12.2%)

2012: 20.16 million bodies (+28.5%), 30.4 million lenses (+16.9%)

2011: 15.69 million bodies (+21.7%), 26.0 million lenses (+19.9%)

2010: 12.89 million bodies (+30%), 21.69 million lenses (+34.7%)

2009: 9.91 million bodies (+2.2%), 16.1 million lenses (+2.5%)

2008: 9.7 million bodies (+17.4%), 15.7 million lenses (+25.6%)

2007: 8.26 million bodies, 12.5 million lenses

July 2023: Units & Shipped Value (all comparisons to YTD 2022):

DSLR Units : 681K -32% YTD

DSLR Shipped Value: ¥31.4 billion -34% YTD

Mirrorless Units: 2.5m +19% YTD

Mirrorless Shipped Value: ¥308.8 billion +17% YTD

Compact Units: 964K -11% YTD

Compact Shipped Value: ¥41.4 billion +22% YTD

Lenses for smaller than 35mm Units: 2.7 million 0% YTD

Lenses for smaller than 35mm Shipped Value: ¥49.1 billion +3% YTD

Lenses for 35mm and larger Units: 2.45 million -6% YTD

Lenses for 35mm and larger Shipped Value: ¥190 billion +0% YTD

Cumulative 2023 Mirrorless unit share (of Mirrorless + DSLR): 78.8% (was 67.8% YTD 2022)

Cumulative 2023 Mirrorless Shipped Value share: 90.8% (was 84.7% YTD 2022)

The ratio of lenses shipped to bodies shipped is 1.6 for YTD 2023. It was 1.7 for YTD 2022.

Full-year 2023 Geographic Share: (Asia doesn’t include China or Japan)

DSLR:

Units: China 11.5%, Asia 07.8%, Japan 3.3%, Europe 41.4%, Americas 34.3%, Other 1.8%

Shipped Value: China 19.2%, Asia 10.7%, Japan 4.1%, Europe 34.7%, Americas 29.9%, Other 1.5%

Mirrorless:

Units: China 26.1%, Asia 15.6%, Japan 10.7%, Europe 21.8%, Americas 21.8%, Other 3.8%

Shipped Value: China 28.7%, Asia 16.3%, Japan 9.1%, Europe 20.6%, Americas 21.1%, Other 4.2%

Compacts:

Units: China 13.7%, Asia 13.8%, Japan 23.9%, Europe 24.2%, Americas 20.3%, Other 4.0%

Shipped Value: China 17.0%, Asia 14.5%, Japan 17.0%, Europe 24.9%, Americas 22.5%, Other 4.1%

Lenses:

Units: China 19.1%, Asia 12.8%, Japan 11.4%, Europe 26.5%, Americas 26.4%, Other 3.8%

Shipped Value: China 21.1%, Asia 13.9%, Japan 10.8%, Europe 24.6%, Americas 25.2%, Other 4.4%

List of participating CIPA companies can be found here.

Via NikonRumors